Why the post-COVID economic recovery will be tech-led

Now more than ever, technology is a linchpin in U.S. economic recovery and resilience. The economic benefits of tech are widespread and take many different forms: innovation is on the rise, research and development continue to drive growth, the sector touts strong job creation, and small businesses are using digital tools to reach customers during COVID-19. In the U.S., tech growth knows no boundaries—a recent study found that the average U.S. congressional district now has 400 high-tech startups. As economic recovery remains top-of-mind for workers, students, and policymakers alike, keep these key points in mind:

— Technological innovation can support workers and small businesses during the economic recovery.

— Online retail and tech are key in sustaining the creation of new jobs.

— Technology’s contributions to economic growth frequently outpace those of competing sectors.

— Artificial intelligence is a bright spot in today’s technology sector, driving widespread economic innovation.

Technological innovation can support workers and small businesses during the economic recovery.

As we look towards economic recovery, it’s important to remember that “no other sector has performed like technology,” notes Emil Skandul in Business Insider. “In the post-recovery period after the Great Recession, tech led US growth in economic output which was also reflected on the stock market. At nearly $1.9 trillion, the sector now generates one-fifth of the total US economy only behind manufacturing and government. All this with over 70% of the sector’s GDP grown in just the past decade… The innovation economy is critical to helping the national economy out of this recession.”

The average U.S. congressional district now has ~400 high-tech startups, showing that tech innovations are making an “outsized” economic contribution, as noted by Jason Oxman of the Information Technology Industry Council. “The technology industry is uniquely positioned to lead the repowering of our economy because it already enables tens of millions of Americans to work, learn, and connect… For U.S. high-tech innovation to truly thrive in the years to come, policymakers must create and sustain an environment in which innovative companies can grow and expand.”

Online retail and tech are key in sustaining the creation of new jobs.

Technological growth and innovation is an “important source of job creation” in the United States, fueling broader GDP growth, notes Jan Rybnicek of Freshfields Bruckhaus Deringer LLP. “The world’s most successful innovators—located predominantly in the United States—have helped to fuel this economic growth by investing to discover new technologies, inventing new business models, developing new products and services, and creating entirely new markets… According to the Bureau of Economic Analysis, the U.S. digital economy accounted for 6.9 percent of GDP in 2017, growing at an annual rate of 9.9 percent since 1998, as compared to 2.3 percent for the economy overall. Technological change also has been an important source of job creation in the United States that has fueled GDP growth. According to one estimate, nearly 12 million people held tech jobs in the United States in 2018.”

Online retail fulfillment can be leveraged for preserving and creating jobs in the “fight against COVID-19,” as highlighted by Christoph Ungerer and Alberto Portugal in Brookings. “E-commerce can help preserve jobs during the crisis. For many restaurants that have had to close during the economic freeze, online delivery services have become a lifeline. Teachers and consultants are continuing to work through video conferencing. In some cases, e-commerce is even creating new economic opportunities. In the United States, Amazon announced that it will hire 175,000 new workers. Online search patterns already give a real-time indication of the role that the digital economy is playing in this pandemic.”

Setting itself apart from competing sectors, online retail has remained a bright spot for hiring during COVID-19, as cited by Michael Mandel from the Progressive Policy Institute and the Wall Street Journal. “The [October] jobs data shows how ecommerce hiring has benefited workers during the pandemic. Since Oct 2019, ecommerce fulfillment and delivery firms have added 262K FTE. Brick-and-mortar retailers have cut 251K FTE, for a net plus. Very few major sectors are in the plus column.”

— “Warehousing and storage companies, which include the sites where workers fulfill online orders, added 28,100 jobs in October, the third straight month of gains.”

Online retail-driven fulfillment jobs often pay more than comparable brick-and-mortar positions, effectively working to “reduce the income gap,” as demonstrated by Michael Mandel of Progressive Policy Institute. “Ecommerce is a net job creator, rather than a job destroyer. Our research shows that ecommerce created 400,000 jobs from December 2007, the last business cycle peak, to June 2017, while brick-and-mortar retail has lost 140,000 full-time-equivalent jobs over the same stretch. Many of these new ecommerce jobs are in fulfillment centers, which are typically counted in the warehousing industry, but bear the same relationship to ordinary warehouses as jet planes bear to bicycles… fulfillment center jobs pay 31% more, on average, than brick-and-mortar retail jobs in the same area… A bigger share for ecommerce has the effect of significantly reducing the income gap, not increasing it.”

Technology’s contributions to economic growth frequently outpace those of competing sectors.

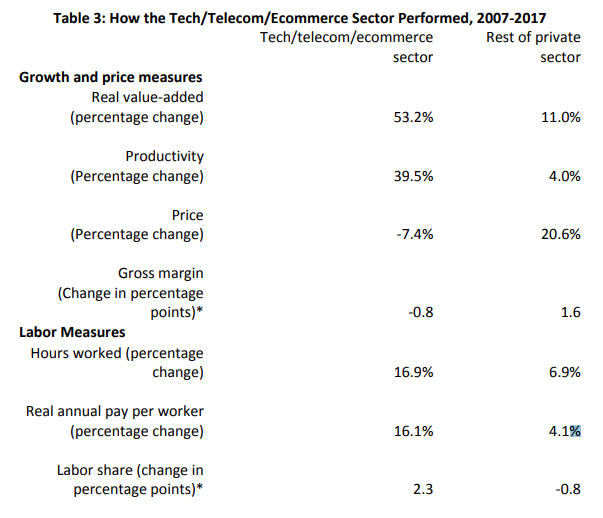

PPI’s Michael Mandel finds the tech sector has “outperformed” the rest of the private sector, suggesting competition in the tech sector is fierce and beneficial for overall growth. “The TTE sector has outperformed the rest of the private sector on every macroeconomic indicator. Indeed, the evidence suggests that to the degree that there are competition problems in the US economy, they are more likely to be found outside the TTE sector.”

As highlighted by Rani Molla in Vox, Tech companies outspend all other U.S. companies when it comes to R&D. “Tech companies lead top U.S. companies in R&D spending. That’s notable because spending on research and development is a key indicator for U.S. productivity, a measure of how well our economy is doing, and productivity has been decreasing lately… spending on R&D is another factor in measuring productivity, and tech companies are certainly contributing in that area.”

Robert Atkinson, President of the Information Technology and Innovation Foundation, writes in a report that R&D spending’s positive impacts on productivity are “economy-wide.” “The principal source of technological progress is R&D. Zvi Griliches’s seminal empirical work on identifying the effect of R&D on productivity found a significant positive relationship between R&D and productivity. A review of economic studies finds that when firms increase R&D investment by 1 percent, their productivity increases by 0.05 to 0.25 percent, or the equivalent to a 20 to 30 percent return on investment. Kancs and Siliverstovs showed that R&D increases firm productivity with an average elasticity of 0.15. An earlier review by CBO found smaller estimates with an elasticity of between 10 and 20 percent for firms and industries, with the rate of return for firms between 20 and 30 percent. However, firms and even industries are unable to capture all the benefits of their own R&D. As such, economy-wide impacts will be higher than firm and even industry impacts.”

Artificial intelligence is a bright spot in today’s technology sector, driving widespread economic innovation.

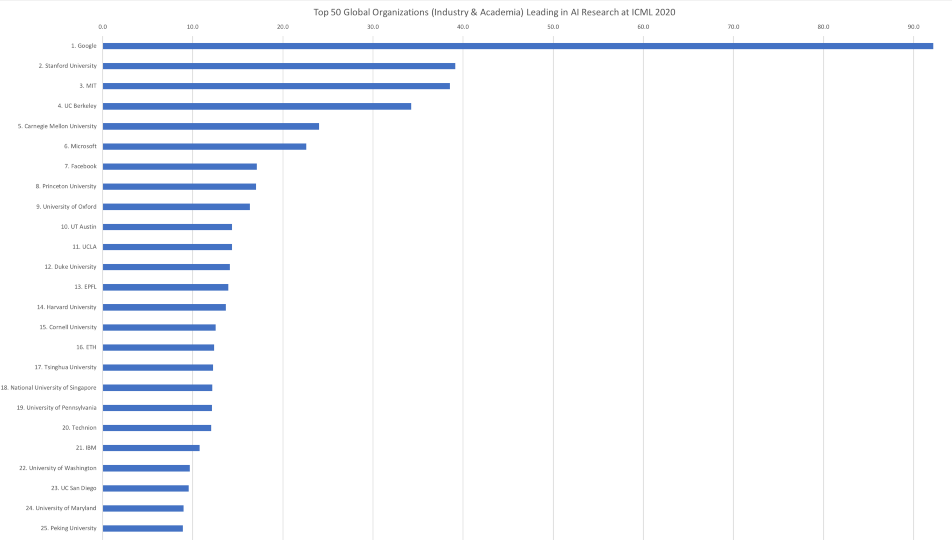

Leading tech services are spearheading fundamental research in artificial intelligence and leading most major universities, as shown by Gleb Chuvpilo, Managing Partner at Thundermark. “The Top 5 global organizations leading in AI research are still Google, Stanford University, MIT, UC Berkeley, and Carnegie Mellon University. Each one of them significantly increased their Publication Index at ICML 2020: Google published an equivalent of 19.4 more papers at ICML 2020, Stanford University is up by 14.7, MIT is up by 15.4, UC Berkeley is up by 10.0, and Carnegie Mellon University is up by 4.8.”

— “The openness of the likes of Google and Facebook to publishing internal research at the conferences created a thriving ecosystem (and a rotating door of sorts) for top AI researchers to move seamlessly between academia and industry (think Yann LeCun or Andrew Ng).”

*cropped image

Artificial intelligence is playing a “growing role” in the U.S. economy, as shown by USPTO data and highlighted by Bryan Walsh in Axios. “The number of AI-related patent applications increased from 30,000 in 2002 to more than 60,000 in 2018, while AI’s share of overall patent filings went from a minuscule percentage to more than 15%. AI-related applications also grew across different kinds of technologies, organizations and geographies. The bottom line: Every great economic innovation begins with a patent, and increasingly that means AI.”

As noted by Jim Pethokoukis in AEI, “AI is already helping us climb higher up the tree of discovery and innovation.” “Innovation is important, but how about innovation that generates more innovation? That’s pretty important, too. ‘The historical record makes clear that science depends on technology in that it depends on the instruments and tools that are needed for science to advance,’ economist historian Joel Mokyr has written… The importance of creating new methods of invention should be remembered when thinking about increasing productivity and economic growth.”